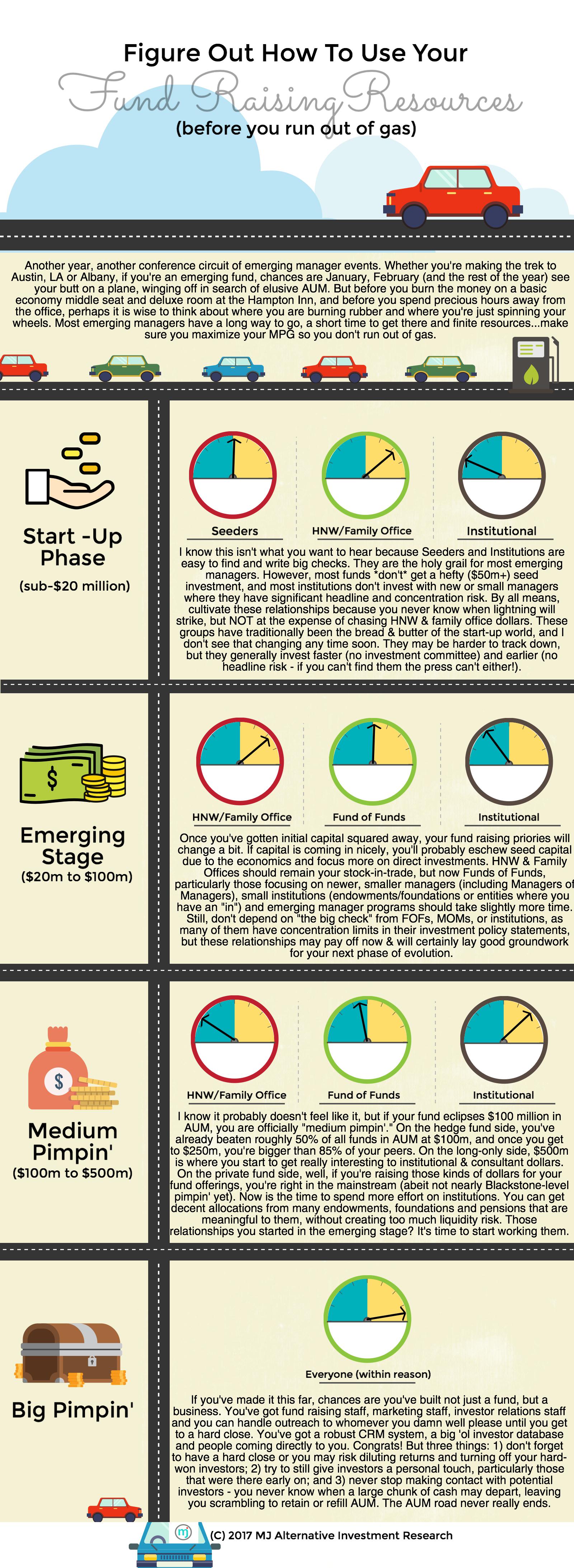

We've all been there.

Moving, shaking, getting stuff done at an industry event.

Hitting up investors for contact details and meetings. Meeting fund managers who can potentially add value to an investment portfolio. Looking for new business prospects among investors and managers.

And then it happens. Knowingly or not, we commit one of the Seven Deadly Sins of Conference Attendance.

Duh duh DUUUUHHHH!

There is perhaps no better way to curtail your most earnest conference efforts than to commit one of the following breaches of event etiquette:

The First Deadly Sin: Chasing Investors Like It's A Zombie Apocalypse

(c) Resident Evil

We all know the shark-to-seal ratio at most investment industry events isn't exactly even. As a result, the investors in the room tend to get a lot of attention. You can see them at cocktail parties, during coffee breaks, or just walking across a room with a trail of hungry investment managers and investor relations folks in their wake. Once, at a GAIM conference in Monaco, they gave out actual proximity detectors to participants. It was like watching the movie Aliens, with investors playing the role of Ripley.

I know every manager that spends money on a conference is hoping to get maximum time with investors, but please, slow your zombie roll. Don't mob investors, and try to keep your interactions to a bare minimum to keep the flow going. You're not going to sell anyone on your fund over a granola bar in a hotel hallway. Keep it simple. Your name. "I'd like to introduce you to my very interesting fund when you have a moment - can I get your card?" Move On. And if an investor is obviously trying to get somewhere (to the coffee, to the can, to a meeting) give them a little breathing room. They'll actually think better of you for it.

The Second Deadly Sin: Hiding From Managers

(c) Mean Girls

Probably as a result of the first deadly sin, some investors have taken to disappearing during networking opportunities (breaks, cocktails and lunches), in the hopes of grabbing a little peace and quiet and piece of mind. As tempting as this may be, it can be beneficial to resist the desire to escape the maddening crowd. I'm assuming that investors go to conferences to find great investing opportunities. Eating lunch in a bathroom stall (ok, your hotel room) probably isn't the best way to find them.

The Third Deadly Sin: Cutting In Line

(c) Family Guy

A panel of investors has just finished up. You really want to talk to one (or more) of the presenters. A line of eager fund managers and conference participants has formed as the panel exits the podium. You wait patiently while they smile, shake hands and give cards to those in front of you. Then, out of nowhere, someone comes up, jumps the line and starts chatting up the investor. Worse yet, the next session starts and everyone has to move to retake their seats, leaving dreams of making contact with those investors unfulfilled. NOOOOOOO! So you. Yes you line-jumping fund manager (or marketer). Don't. The investor knows you did it (even if they can't always stop you). The managers who were patiently waiting know you did it (and are silently fuming). And you just look kind of like a tool. Just say no to line jumping.

The Fourth Deadly Sin: The Nameless Text

(c) Tropic Thunder

You managed to score an investor's card at a cocktail party, lunch or during a break. "What the hell," you think. "I'll send them a text to see if they have time to meet for breakfast or coffee in the morning." So you send a text: "Great meeting you last night. Grab a bite tomorrow am?" The only problem? The investor has NO FREAKING IDEA who you are. For all they know, this message could be a misdial from someone else's beer-goggled evening.

It's never a great idea to text investors anyway, unless you have an imminent meeting or they've given you express permission, but texting without identifying yourself and assuming that the investor will remember you out of throngs of fund managers is just silly. Include your name and the fund name. Or better yet, send an email.

The Fifth Deadly Sin: The Drive By

(c) The Dukes of Hazzard

Similar to the hiding from managers, the drive by occurs when investors, usually those scheduled to speak, attend an event only for their session. Fund managers, lured to pay event fees in part by the hugely cool and monied speaking faculty, get gypped out of their hard-earned dollars and investors get cheated out of finding good investment ideas for their portfolio. A true lose-lose.

The Sixth Deadly Sin: The Close Talker/Cornering Folks

(c) Seinfeld

Conferences are crowded. Conferences are loud. Investors are scarce. One-on-one time is at a premium. That's still no excuse from getting all up in someone's personal space. I have literally been backed into a corner at an event before and, let me tell you, I was not amused. I also once attended a conference after just getting Invisalign. I wasn't entirely used to the Invisalign trays yet, and had just hurriedly scarfed a mint when I was corralled by a fund marketer. Before I knew it, the mint flew out of my mouth and landed on the marketer's arm. I tried to be cool - I picked the mint off of him, said "um, I think this may be mine," and slunk off. But seriously, if you're so close that an Arthur Bell promotional mini-mint with lisp velocity and zero aerodynamics can hit you with enough force to stick to your skin, you are too damn close. An arm's length for distance is a good rule of thumb here.

The Seventh Deadly Sin: No Business Cards

(c) American Psycho

This one can be a bit tricky as both investors and fund managers are at times guilty. Generally speaking, investors eschew business cards to avoid a post-conference email zombie apocalypse, while fund managers and marketers either don't bring them to (Machiavellian interpretation) force investors into giving their cards up, or because (poor planning interpretation) they underestimate how many cards they will need.

Dear All: Conferences are networking events at heart. Bring cards and enough of them. That is all.

So there you have it.

Before you hit up your next Hedge Fund, Private Equity, Venture Capital, Institutional Investor or other industry event, make sure you are up-to-date on conference etiquette, or risk being judged in attendee purgatory.