Think there's not enough evidence to demonstrate that gender diversity can boost returns and improve diversification? Take a look at the infographic below and see if you still feel the same way...

(c) 2015 MJ Alts

Think there's not enough evidence to demonstrate that gender diversity can boost returns and improve diversification? Take a look at the infographic below and see if you still feel the same way...

(c) 2015 MJ Alts

I couldn’t face the same old Thanksgiving this year. Another tryptophan-laced orgy of food combined with marathon cleaning sessions before and after the big event, someone arriving with undisclosed food allergies, red wine on the carpet, cats eating the centerpiece and leftovers I have to look at with the dull eyes of the long married for weeks after the main event. No thank you!

So I did what any sane person would do: I went to Hawaii instead.

There, Thanksgiving was a Pina Colada-fueled homage to my ever present "SPF Burqa", sandy beaches and folks that unironically say “Brah.” I even tried surfing for the first time. And despite my deep-seated pleasure at a) not dying, b) not wiping out a la Greg Brady and the cursed tiki necklace, and c) standing up on at least one North Shore wave, I quickly learned after posting this picture that people did not necessarily share my enthusiasm or revel in my surfing accomplishments.

No, the most popular picture I posted was instead this gem, where a legion of people could see me wiping out like a boss.

I can’t claim to be particularly unique in this regard. In fact, it seems like the whole world likes nothing better than a deep dose of what the Germans would call schadenfreude, or “pleasure derived by someone from another person’s misfortune.” My full-on, Pacific Ocean-surfing-netti-pot photo was an exhibition of this lovely phenomenon writ small, reserved for those brave enough to call me “friend” on Facebook.

For a larger scale demonstration of schadenfreude, we had only to look as far as the hedge fund headlines in the last ten days or so. Some of my personal faves include:

“Hedge Funds Lick Wounds After Tough Year”

“Another Humbling Year For Hedge Funds”

“Hedge Funds Brace for Redemptions”

“Hedge Fund Giant Laments Profitability, Will Return $8 billion”

“Surprise! Hedge Funds Aren’t That Bad At Picking Stocks”

“The Incredible Shrinking Firms of Hedge Fund Billionaires”

Yeah, yeah, yeah…let’s all agree 2009 to present hasn’t been the easiest time to be a fan of alternative investments.

But let’s take a moment to put our keen delight in the misfortune of hedge funds into perspective.

Hedge funds aren’t exactly wiping out Greg Brady-style, either.

1) Yes, there have been closures & return of capital from some hedge funds, including a few large enough to be household names. BlueCrest opted to return outside investor capital, transitioning to a private investment partnership due to redemptions, fee pressure and its impact on recruiting. Avenue shuttered its hedge fund in favor of longer duration investments. Blackrock closed a macro fund that was down single digits for the year. Seminole returned $400 million of investor capital to better align the trading strategy with the markets and protect profitability, after returning 16% on average for the last 20 years. None of these are the spectacular, cry-during-an-MTV-performance, Justin Beiber-style meltdown, but rather strategic decisions we expect business owners to make daily.

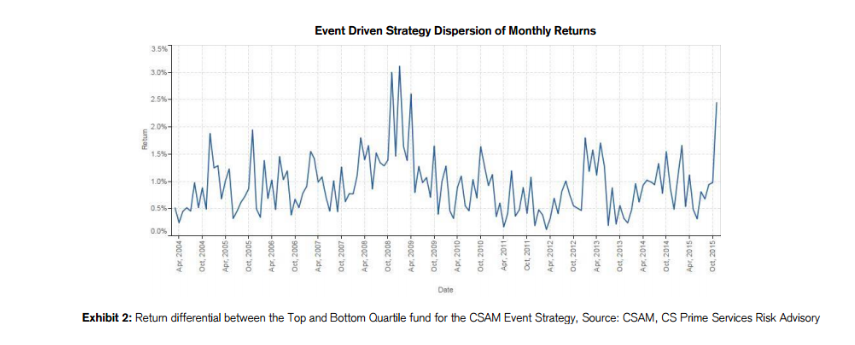

2) Yes, hedge funds haven’t exactly set the world on fire with 2015 performance. Or 2014 performance. Or 2013 performance…well, you get the picture. However, we have to remember, yet again, that the comparisons we’re making are average performance. If you look at return dispersion (here from Credit Suisse) even within single strategies of hedge funds, it is easier to remember that there are funds performing much better than the “average.”

(c) Credit Suisse Asset Management

3) Yes, hedge fund managers are losing money, but perhaps so are you. Given the explosion of institutional assets in hedge funds, celebrating the losses of a hedge fund could be tantamount to celebrating the losses of your favorite school teacher, fireman, police officer or other “main street” investor. And if that don’t take the wind out of your sails, I don’t know what will.

However, even with these clarifications, I am perhaps a little overdue in providing some hedge fund “tough love.” So here goes:

Hedge fund managers: Fee pressure is a pain. Expenses are up, regulation is increasing, the markets are more difficult to navigate and profitability is down. It’s unlikely that many of you will be able to weather a protracted double-digit or high single digit drawdown given the economic realities of managing a fund today and you’re less likely to be given the benefit of any doubt now than at perhaps any other time in hedge fund history.

But what protects fee structures and prevents increased regulation? Generating returns for your investors and doing the right things (disclosures, filings, investor relations, any and all regulatory filings) and doing it in a way that lets you sleep at night. This could be a watershed moment for hedged asset management. I wish I had a magic wand that would make it all easier but instead I can only say, for the love of all that’s holy, get ‘er done.

Writing headlines is hard.

Coming up with something appropriately attention grabbing without veering off into purple prose is a serious skill. I, myself, occasionally have moments of headline genius, but often times wind up more in the land of "huh?"

And I know it's not just me. After all, the Washington Post just gave us this headline gem last week.

Best. Headline. Ever.

But really, the world of hedge funds deserves their own set of headline awards. The headlines about the hedge fund industry are often incendiary, divisive and generally geared to just stir stuff up.

In order to help casual readers of hedge fund press wade through the copious and inflammatory rhetoric, I've created a handy-dandy hedge fund babel fish for y'all below.

May this little translation tool reduce your drama factor exponentially this Thanksgiving, even if you use it while hiding away from kids/in-laws/friends/siblings/spouses or dishwashing duties.

(c) MJ Alts

Happy Thanksgiving to those that celebrate it, and may everyone find something this week for which to be grateful, whether there's tryptophan involved or not.

Those of you that have heard me speak on more than one occasion have probably heard me utter the phrase "Investing in emerging managers is like sex in high school. Lots of talk, very little action." In full disclosure, Jim Dunn of Verger was the first to utter those words, but they are so apropos that I have sense borrowed them for myself once or twice. (Thanks Jim!)

This week, I had the opportunity to informally poll investors and emerging managers, this time in the form of women-run funds, and that wonderful turn of phrase proved apt once again. In fact, I could almost hear Mike Damone saying "I can see it all now, this is gonna be just like last summer. You fell in love with that girl at the Fotomat, you bought forty dollars worth of [freakin'] film, and you never even talked to her. You don't even own a camera."

Indeed, it does seem as if investors often spend a lot of time stalking the camera store, but never getting the picture. So I decided to ask the audience of managers and investors at last weeks 100 Women in Hedge Funds Senior Practitioner Workshop where we stand and what could help the situation. Here's what I learned.

(c) 2015 MJ Alts

(c) 2015 MJ Alts

(c) 2015 MJ Alts

(c) 2015 MJ Alts

And, while these responses were specifically geared towards women owned and women run funds, in my conversations with investors, the issues are not entirely dissimilar for minority owned and run funds, or really any other emerging manager.

So, ladies and gentlemen, let's work the problem and see if there aren't good solutions to these issues. It will be healthy for me to have to come up with a new, creative and vaguely offensive way to describe the industry.

And please take a moment to support 100 Women in Hedge Funds as they are part of the solution and the reason I could run this quirky poll in the first place!

I had yet another wedding to attend this weekend: My third in four weeks. I may never get all this rice out of my hair. Seriously.

But as I was driving to this happy event, a few questions rolled through my mind:

Was I dressed appropriately? (Not really.)

Was I going to make it before the bride actually walked down the aisle? (Just barely.)

Would there be a reprise of my “Footloose Dance” humiliation during the reception? (Thankfully, no.)

And then a strange thing happened. As I cruised onto the Ashland City Highway, a familiar tune pulsed from my speakers.

“An' I don't give a damn 'bout my reputation

The world's in trouble, there's no communication

An' everyone can say what they wanna say

It never gets better, anyway

So why should I care about a bad reputation anyway?

Oh no, not me, oh no, not me”

Yes – Saint Joan Jett had arrived to calm my nerves before I rushed into the small rural church, just in time for the wedding. To say I rocked those last five minutes of the drive would be an understatement.

When I awoke on Sunday morning, I was faced with a somewhat similar scenario. Hedge funds were skewered yet again; this time in an article by the New York Times referencing a study of eleven pension funds entitled “All That Glitters Is Not Gold.”

The study demonstrated that hedge funds had added little value to public pension funds (in many cases underperforming the fund as a whole) and cost an exorbitant amount, based on the authors’ arbitrary 1.8% and 18% fee structure.

The report concludes: “Although hedge fund managers have convinced many investors that they provide investment products so uniquely profitable that extraordinarily high fees are warranted, our research suggests that there is little evidence to back up these claims.”

Oh joy. Seems I’m not the only one that needs to be concerned with my reputation.

But, upon further study of the report, I noted a couple of interesting points that are, I think, at least worthy of consideration.

Time Periods Matter: Of the eleven pension funds reviewed for the study, nearly half included only the bull market period that started in 2009. There was no period longer than 13 fiscal years in the study (about the time the first pension funds dove into the hedge fund waters), and actually only one of those. For the pension plans that did include the 2008/09 fiscal year, in every case, based on visual interpretation of the line graphs, the hedge fund portfolios outperformed. So it would appear that, given the appropriate market environment, hedge funds can and do perform. So should we draw concrete performance conclusions on hedge funds’ performance during what has been a raging bull market? As we all know, if a fund is truly “hedged” it is nigh on impossible for that fund to outperform a market with its foot on the gas.

Manager Selection Matters: As investors, we make choices about our investments. Our choices are informed by the amount of money we have (or don’t have) to invest. They are informed by investment bylaws and state regulations. They are informed by the universe of investment options of which we are aware. They are informed by the amount of time we have to devote to our investment research. They are informed by our behavioral biases and those of other key decision makers. In other words, fund selection isn’t straightforward. Think about how hard it is to order a great entrée in a restaurant – and now picture that entrée costing thousands or millions of dollars. Get my drift?

No matter how you look at it, each investor has some responsibility for their fund selection. What’s interesting about this study is, again, based on eyeballing the line graphs, it looks like the plans reviewed generated hedge fund returns of about 8.3% in FY 2014. If you look at the NACUBO/Commonfund review of 832 endowments, in contrast, you see that they averaged a 9.9% return from “marketable alternative strategies.” Now, granted there could be a difference in terminology, or there could be something there. After all, I always say in investing, Your Mileage May Vary, and manager selection is a huge part of that. Even among the eleven managers in the "Glitters" study, there is a large variance in overall portfolio and hedge fund performance.

So maybe the problem isn’t the investment vehicle. Maybe there is something that public pensions and others that are disappointed with their hedge fund earnings could learn or adapt from public endowments' approach to hedge fund investing. After all, endowments entered the hedge fund fray a bit before their public pension brethren. And, now this is just a thought, but looking at the largest endowments in the NACUBO study, they’re kind of kicking ass when it comes to hedge funds. Their marketable alternatives strategies returned 11.4% in FY’14, well above hedge fund industry averages and well above what others may be experiencing. What’s the what here? Should we be looking to those investors to figure out what ingredient we may be missing from our own secret sauce? It's not that the pensions included didn't do an admirable job of building portfolios, as each beat the overage hedge fund average, but is there something that could be done (structurally, in manager selection or otherwise) to boost returns?

Fees, Fees, Fees: As I mentioned, the study uses an arbitrary 1.8% and 18% fee structure, even though we know that industry average is closer to 1.5% and 17%, but let’s even leave that aside for a moment. We really have no way of knowing what these pensions paid in fees unless it is publicly disclosed. If they went into a separate account, for example, they may have a totally different fee structure. If they negotiated a lower fee, that’s also difficult to know. In many cases, public pension “big dogs” are able to achieve fee concessions that us mere mortals cannot hope to get.

Does this mean I think there’s no wiggle room for hedge fund fees? Absolutely not. Those of you that are regular readers know that I generally support sliding scales for management fees in particular, based on the manager’s total AUM. But even then, it’s not a straightforward “Off with their fees!” equation. Some strategies are more labor intensive than others, which may require higher fees. Newer and smaller funds have very little room between profitability and problems in their fee structures. As in most things hedge fund related, there is not one-size-fits-all fee solution. Investors should advocate for themselves within reason, and managers should protect their ability to attract talent, execute strategy and generate returns for all their investors. It’s all about balance.

It’s perhaps wise, then, to take a step back and think about whether we have enough data to draw actionable conclusions and, perhaps more importantly, if there is a way to improve hedge funds relationship and return contribution to public pensions. Anything else would be discarding the baby with the bathwater, based on what looks like a bad reputation.

Less than one score and seven years ago, it was relatively easy for hedge funds and other private fund vehicles to gain early stage capital. They went to their networks of high net worth individuals, let a little word of mouth work its magic, and then waited for early investments to roll in. Due diligence was minimal, who you knew was paramount and a rising tide (the Bull Market) lifted all ships. If it hadn’t been for the shoulder pads, it might have been the golden age of hedge funds.

Now, of course, raising early stage capital is a whole different ballgame. From seeders to bootstrapping to joint ventures to Founders’ Share classes, there are a host of options available to emerging managers who want assets, although frankly most work better in theory than they do in practice.

Lately, most of the buzz has surrounded Founders’ Share capital. And for managers that are unable to secure bulk early stage financing from a seeder, founders’ shares may hold some appeal.

Founders’ shares generally reduce management fees by up to 50 basis points, while incentive fees may be reduced by up to 5 percent. Founders’ shares are generally offered for a limited time for only early mover investors and are discontinued when a specific asset level or time threshold is passed. Founders’ Shares, and their reduced fees, remain in effect as long as the investor maintains an allocation to the fund.

Founders’ Shares have a lot of perceived benefits, including:

However, just because they sound good in theory doesn’t mean they are a panacea for every fund.

Perhaps most importantly, it’s important to remember that sacrificing fee revenue is most dangerous when assets under management are low. Once a firm or fund has attracted $1 billion in AUM, even a 1% management fee will generate $10 million in fee revenues in a flat year. For a $100 million fund, that fee revenue falls to $2 million in a 2% and 20% scenario, and $1 million in a 1% and 20% scenario (assuming flat performance).

And of course, those numbers are BEFORE expenses. Citibank estimates that a typical $100 million hedge fund must spend $2,440,000 each year to keep the fund running. Factoring that into the equation, it’s easy to see how quickly a fund can go from hero to zero, particularly if performance doesn’t pan out.

(c) 2015 MJ Alts

So I said all that to say this. Founders’ Shares can be a great thing if used judiciously, but please do the math to determine how much of a great thing you can stand to offer.

During an unbelievable number of meetings with investors and managers, I hear the same two refrains:

“We’re looking for the next Blackstone.”

Or

“We think we’re the next Blackstone.”

It’s enough to make you wonder if such success is commonplace or if we’re all overreaching just a teeny bit.

Well, I’ve shaken my Magic Eight Ball and the answer is this, at least for newer funds: “Outlook Not So Good.”

Recently, on a boring Sunday afternoon, I decided to go through Institutional Investor’s list of the 100 largest hedge funds and figure out when each fund company launched.

Yes, clearly I need more hobbies.

But the results (as well as my lack of social life) were pretty shocking. There are no funds within the top 100 that launched during the last 5 years. There are only 4 funds in the top 100 that launched within the last 10 years. In fact, nearly 70% of the top 100 hedge fund firms launched before the first iPod.

Obviously, this begs a question: Where are all the new Blackstones?

(c) 2015 MJ Alts

Whatever complaints can be lobbed at hedge funds, I do find it hard to believe that the talent pool has deteriorated to such a degree that there just isn’t a supply of skilled fund managers available. On the other hand, I do have a few theories on what forces may be at work.

This is not to say that newer funds haven’t made it into the “Billion Dollar Club” or that rarified air of 500 or so hedge funds that manage the bulk of investor assets. It is, however, a stark look at how we define expectations and success on both the investor and manager side of the equation. If 40 is the new 30 and orange is the new black, is $500 million or $1 billion in AUM the new yardstick for hedge funds? Time will tell, but I’m wondering if the Magic 8-Ball isn’t on to something.

As I prepare to move from one demographic checkbox to another later this week, I’ve been spending a fair amount of time wandering down memory lane. I’ve re-watched the movies from my youth, including Sixteen Candles, Ferris Bueller’s Day Off, Caddyshack and Smokey & The Bandit. I’ve gotten in touch with my inner Carlton Banks during a stirring, post-wedding live band rendition of “Footloose.” And I’m pretty sure when Loggins sang “everybody cut, everybody cut, everybody cut Footloose!” he wasn’t talking to me.

Property of Fresh Prince of Bel Air.

I’ve also spent a lot of time thinking about all the things I know now and all the stuff I have yet to learn.

For my 45th year, I plan to keep learning as much as possible. I’m going to surf camp for a week. I will finally learn how to do a proper figure skating sit spin. I vow to discover how to drive with more limited use of my middle finger. And of course, I hope to continue to figure out how to be a better investor, researcher and snarky advocate for the alternative investment industry.

When reflecting on what I do know I know, however, I did come up with some truths that constantly guide my investment decisions and unsolicited advice. They’ve become the North Star of my investment world, so to speak. And as luck would have it, there’s exactly one for each decade, with one to grow on. How fitting!

One: Continuous outperformance is a myth. Every manager screws up, gets caught with their portfolio pants down, or otherwise loses money from time to time. Finding the managers that minimize those downturns, can admit to and learn from mistakes, doesn’t keep making the same mistakes and, perhaps most importantly, live to invest another day is the real trick. Frankly, the only managers I’ve ever seen that never posted losses were frauds or, um, otherwise a bit creative in how they marked their portfolios.

Two: Between investing early and late, I’ll take early any day. In 2006, I started researching the outperformance of emerging managers. In 2010, I started researching women and minority run funds. Thus far, investors have largely ignored those groups in favor of the same old, same old. As an investor friend of mine once quipped: “Investing in emerging managers is like sex in high school, even though everyone talks about it, no one actually does it.” Despite the lack of investors putting their money where my mouth is, I remain convinced there’s significant alpha to be had with these groups. The lesson? Just because the packaging doesn’t look familiar doesn’t mean there’s not goodies inside. The same thing goes for new trends for venture capitalists, out-of-favor investments, sectors or strategies. Early bird, meet worm.

Three: Any way you can invest involves risk. Whether you keep money in a checking account, invest in hedge funds, index funds, actively, passively, in real assets, conservatively or aggressively, there is a risk you will lose money or not make enough money, or that you will not have access to your money or otherwise lose out. My Grannie kept money stuffed in the pockets of the clothes in her closet because she thought that was risk free, but she missed out on any potential profits and, obviously, her returns lagged inflation. Not to mention: what if the house burned down? There are no risk-free investments. Period.

Four: Investment professionals (and anyone else) that truly want to rip you off will find a way to do so. Having said that, the best way for them to accomplish that is to build blind trust. After all, the “con” in con artist is short for confidence. Most of the big scams in investing couldn’t happen without trust, and most of the time those closest to the bad actor are the first to get victimized. Think Bernie Madoff who bilked members of his religious community and other friends and family. Obviously, you need to trust your investment professionals by all means or you’ll never sleep at night, but never forget to at least periodically verify.

And one to grow on: Look out for zebras, but don’t forget about the horses. A recent venture capital fraud case involved not a sophisticated cyber fraud or complex skimming techniques. The perpetrator merely added a “1” to a check, changing $8 million to $18 million. Occam wasn’t wrong: It’s not always the most sophisticated schemes or black swans that cause losses. Sometimes the ordinary can be just as dangerous.

What’s the biggest lesson you’ve learned in your investing career? Feel free to sound off in the comments below with your best advice. And please follow me on Twitter (@MJ_Meredith_J) if you prefer your snark in 140 characters or less.

As a relatively new Tweeter (Twitterer?), I sometimes get questions from followers on a host of topics. In case you were also wondering, here are a few recent answers: Yes, there are almost always song lyrics hidden in my blogs. Actually, my hair is naturally large & no outside intervention is required. And yes, creating this much snark and sarcasm is exhausting.

Last week, I got the following question Tweeted in my general direction:

And while I can’t guarantee maximized profits, dear Tweeter, I can offer a few suggestions to enhance your first foray into alternative investments:

Take hedge funds, for example - they aren’t all gypsies, tramps and thieves, whatever you may have read. Fees are closer to 1.5% and 18% than to 2% & 20%. The vast majority of hedge fund managers make nowhere near the $11.3 billion that the 25 largest funds rake in, and are much more sensitive to reductions in fee income than you may think (see also http://www.aboutmjones.com/mjblog/2015/6/29/hedge-fund-truth-series-hedge-fund-fees). Insider trading happens, but is remarkably consistent at about 50 enforcement actions per year (across all miscreants, not just hedge funds). Ponzi schemes have happened but rarely at serious scale (and no, Madoff was not a hedge fund). Average performance of hedge funds has been lackluster but the top performers (who I’m pretty sure are the folks you want to invest with anyway) have generated some outstanding returns, even in the last few years. Don’t believe me? See the distribution of return graphics from Preqin’s latest study.

Finally, there is no proof that hedge funds cause cancer, despite what the Hedge Clippers may say.

2. Get a good data sample – One of the key mistakes I see from new investors in alternative investments, especially hedge funds, is the lack of a good data sample. The thing about hedge fund data is there is no requirement for any fund to report any information to any commercial hedge fund database. Period. As a result, the data is fragmented and incomplete. The only incentive for a fund to report to a database is to pursue assets. If a fund isn’t in asset raising mode, has a hearty network of prospective investors, or if the performance of fund is unlikely to attract assets, many funds simply won’t report. In addition, many funds report to only 1 or 2 databases, and if those don’t happen to be the ones to which you have access, well, that’s just tough cookies. The moral of the story? Invest in data. Buy data and gather information on your own by networking, going to conferences and talking to other investors about what and who they like. The only way to ensure you make the best investment decisions is to know what your options are in the first place.

3. Think about what risk means to you – All too often, we try to boil risk down to a single data point. Whether it’s drawdown or standard deviation, we attempt to quantify risk because we feel like what we can quantify we can understand and control, right? Wrong. Risk means different things to different people and each investor will maximize different aspects of risks. For example, one investor may feel their biggest risk is not achieving a certain minimum acceptable return. Another may feel their biggest risk is losing a substantial amount of their investment. Yet another may feel headline risk is their biggest concern. And still another may worry about liquidity. The list is endless. The important thing for investors is to think about their personal (or organizational) definition of risk before making an investment, then identify the risks in any investment strategy as thoroughly as possible and finally determine if the potential upside is worth taking those risks. All investments involve risk. Period. Deciding whether the risk you’re taking is worth taking is up to you.

4. Get your nose out of your DDQ – Get to know a manager and his or her team not just by grilling them with a long due diligence questionnaire, but by having a real conversation. If you know what’s important to a manager, what drives them, what keeps them up at night, how they got to where they are, what influences them, and how THEY perceive risk you have a much better chance of developing the rapport and trust that is necessary to any successful investment.

5. Look ahead, not behind – If you’re chasing returns, you are already behind.

6. Watch out for dry powder and Unicorpses – There is an awful lot of money flowing into private equity and venture capital and a finite number of reasonably priced deals, great management teams and fantastic business plans. Ensure any GP you plan to LP has the DL on deal flow.

7. There is no I in TEAM – Actually, there is – it’s in the “A” holes. But I digress. My point is there is a lot of work associated with finding and doing due diligence and ongoing monitoring on alternative investments. If you don’t have a robust team, it’s ok to go to folks for help. Funds of funds, outsourced due diligence, OCIO, multi-family offices, operational due diligence firms, and other providers can be a lifesaver to a new or small investor in alternatives. It may not be cheap, but neither is recruiting, training and providing salary, bonus and benefits for an entire specialized team. Weigh what you can do in house against what you can easily outsource and spend the most effort on the voodoo that you do so well and money on the stuff that isn’t the best use of your time or expertise.

So there you have it: A small list of tips to help with first (or continued) forays into alternatives. Got a tip of your own? Put them in the comments section below.

I learned two important lessons from writing my book: Women of The Street: Why Female Money Managers Generate Higher Returns (And How You Can Too).

At the height of my book-induced anxiety, I decided to try an experiment. I decided that I would stop focusing on typos, PR, and what people would think of my research and that I would instead focus on other people. Hopefully, by doing good deeds for others I could do good and do well at the same time.

I kept a running list of my daily good deeds. I bought a massage gift certificate for my hair stylist (if you had to mess with my hair, you’d deserve one, too). I took a milkshake to a friend in the hospital. I bought Starbucks for 3 strangers behind me in line. I chased a neighbor’s loose dog down the street and brought it back to its fenced-in yard. I worked with charities and stray animals. I donated to good causes and I gave folks home-grown tomatoes (as every good southerner should do).

And guess what? At the end of the day, I knew I had made a difference. And I felt better. The folks around me felt better and, although the impact was, I’m sure, small, it was something.

Because of the research that I’ve done around diversity and investing, I often get asked how we can increase the number of women (and minorities) in the investment ranks, and I’ve spent a lot of time pondering the solution.

As I was reflecting recently on my own mission to create positive change, I realized that the answer to the diversity conundrum may not be that dissimilar. Perhaps we can effect change with a basic concept that we’re all extremely familiar with. Let’s Compound Diversity.

We all know how critical mentoring is to success in this industry. There isn’t a single interview in my book that doesn’t at least mention the presence of at one significant (male or female) mentor. But we also know that mentoring is a time consuming task. And that often, the process starts too late, after the diversity funnel has already begun to narrow.

So instead, let’s focus on what I like to call “Mentoring Moments.” These are opportunities for you to help a women advance that don’t require a year-long (or life long) commitment, but which still can have an enormous amount of impact within your firm and across the industry.

(c) 2015 MJ Alts

It’s when you can include a junior woman in on a sales pitch, due diligence, or board meeting they might otherwise not be invited to.

It’s when you email a job description to your network to help ensure that at least one woman has a seat at the interview table.

It’s getting an extra pass to a conference and giving it to a junior colleague who might not otherwise be selected to go.

It's ensuring that diverse firms have a seat at the table when competing for investment mandates, and awarding that mandate if that firm is the best fit.

It’s when you send a firm-wide email about someone’s great work that might otherwise go unnoticed or unsung.

In short, it’s the million little ways you can help advance women and minorities in finance and build diversity in the industry.

But mentoring moments don’t end at work – they can and should happen outside of the office as well so that we increase the number of girls and women that are potentially interested in finance and investment to begin with.

In a prior blog, I discussed how girls are less likely to get an allowance than boys and that girls are less likely to be paid for chores than boys.

I showed statistics that pay disparity starts early, with girls making less for the same chores. Boys even make more for babysitting, despite the fact that 97% of all babysitters are female.

Girls also report that they are less likely than boys to be talked to about how to finance college or budgeting or other money matters.

So start your mentoring moments early. With allowances, and discussions about what you do at work and college funding and career progression. My mom made me do little pop quizzes in math (Quick! Convert that mile marker to kilometers!) when I was a girl to ensure I was never intimidated by numbers.

Picture this: A fellow panelist at the CFA Women’s Conference in San Antonio caught her daughter and her friend playing dress up and asked what they were getting ready for. Her daughter’s answer? “We’re going to a board meeting.”

Amen.

It’s our job to help future financial professionals that may not look like the ones you normally see on CNBC know that investing is cool, and that because you’re helping other people achieve their financial goals, can be also looked at as doing well while doing good.

And if everyone (male and female!) who reads this blog commits to just five mentoring moments over the course of the next year, think of the difference we can begin to make. Your five mentoring moments will compound, and 200 mentoring moments, and, with luck, those moments will continue to compound as those women and girls embark on their own mentoring moments. And thus, the Compound Diversity movement takes hold.

We can make a difference. One moment at a time.

If you’re willing to take the challenge I’ll even make it easy for you. Here’s a form you can print and fill in as you accomplish your five mentoring moments. First one that fills it in and sends me a copy gets a copy of my book and a bottle of small batch, super tasty Southern bourbon, on me.

(c) 2015 MJ Alts

One of my favorite movies is The Princess Bride. Those of you that know me and my sense of humor probably aren’t surprised by that, but seriously, how can you NOT love a movie with R.O.U.S. (Rodents of Unusual Size), Miracle Max and a mysterious six-fingered man?

In fact, one of the best movie exchanges ever written probably appears in that movie. In it, the Dread Pirate Roberts is following Vizzini, Fezzik, and Inigo Montoya as they kidnap the titular princess, intent on malfeasance.

Even as the Dread Pirate Roberts pursues them across an ocean of screaming eels and up the Cliffs of Insanity, Vizzini cries repeatedly that such actions are “Inconceivable!” Finally, Inigo Montoya declares: “You keep using that word. I do not think it means what you think it means.”

Comic gold? Absolutely.

Applicable to the alternative investment industry? Curiously, yes.

Recent interactions with various folks in the investment industry have led me to believe that Inigo may well have been speaking to us as well. In a number of cases, the words we use don’t mean what we think they mean. Perhaps we’ve selected them because they’re particular sexeh or they represent what we wish were true, rather than what is true, but regardless, we’re all sometimes guilty of creating a little linguistic anarchy by misusing investment terminology.

So, without further ado, and in no particular order, here are my top five investment terms that do not mean what we sometimes think they mean.

Seeing and hearing these terms misused in the investment industry makes my left eye twitch. Help save me from a lifetime of folks asking “Are you looking at me?” and start using these frequent used, but often abused, terms correctly.

Sources: http://www.globaleconomicandinvestmentanalytics.com/archiveslist/articles/499-the-case-for-high-conviction-investing.html, Merriam Webster, CB Insights

It’s funny, but I have a lot of conversations about all the travel I, and my fellow investment professionals, do in the course of our daily lives. For some reason, telling people that you “have” to go to New York, Los Angeles, Hong Kong, London, Paris, Monaco or some other “sexeh” locale puts all sorts of weird ideas into people’s heads. It’s like they think business travel turns you into P-Diddy or something. You’re big pimpin’ and you spend the cheese because you go to New York and stay at the W Hotel in Times Square for a night (Starwood whore!).

So, for those of you who wonder what all us lonely travelers do when we’re out on the road, I thought I’d sum it up for you. If either scenario sounds familiar to you, sound off in the comments section.

My (first class) flight leaves at a completely reasonable daylight hour. I was able to pack during work hours and therefore had no encroachment upon my “personal life.”

I arrive at the airport and whisk through security ‘cos, you know, frequent flyer street cred.

I board the plane and drink champagne or my alcoholic beverage of choice all the way to my destination, where I am picked up by a helicopter or limousine and deposited at my uber-chic hotel.

My first meeting is always a lunch meeting, which is somewhere swanky and leather and where martinis are swilled until it’s time for my next meeting, which, curiously, is also over drinks.

After that meeting I return to the hotel to return a few calls. Or nap. Or get a massage. You know…”work.” Maybe I even take time to sightsee or catch a show.

My dinner meeting is always somewhere fabulous that the average mortal can’t get into and where my meal costs more than a mortgage payment.

Everyone then adjourns somewhere similarly hip/swanky (depending on the friend) and then finally return to the hotel around midnight.

The next morning starts no earlier than a brunch meeting before I head to the world’s largest board room to make a presentation about how everyone secretly makes money but doesn’t tell “the little people” about it.

I then go to another lunch meeting, knock back a couple of drinks before collecting checks totaling eleventy-million dollars and boarding my (first class) flight home, having skipped security entirely because, let’s face it, I’m me.

I almost never get a flight that leaves when it’s daylight. Whether that means I get up at the absolute crack of dawn or whether that means I schlep my bags to the office and work all day before racing to the airport to catch a flight that night, I rarely see the outside of an airport while the sun shines.

The whole time I’m en route to the airport, I am checking to see where I am on the upgrade list. However many first class seats are left, there is at least a 50% chance that I am that number plus one.

I do have TSA Pre-Check, but I seem to have a high “hit rate” for random extra screening. So I get often get felt up before boarding the plane. And it’s Nashville, so there’s often someone with a gun in the pre-check line. After security I rush to take my seat and put my earphones in (and/or feign sleep) before my seatmate can strike up a conversation about insurance, actuarial work, healthcare or some other topic I could care less about.

I arrive at my destination city and get in a cab. It usually smells like Fritos. Unless it’s been raining in which case it smells like O that didn’t stay with the B. And Fritos. (C’mon y’all, that helicopter thing was like TWO TIMES and it only happens for GAIM Monaco).

I drop by the hotel (which is either corporate or points-grabbing approved), but my room isn’t ready because it’s still WAY early to check in. I store my bags and run to my first meeting.

(Full disclosure: Sometimes I check in so late that the only rooms left are “accessible”, so I get to hang my clothes 3 feet off the floor…almost equally fun).

I generally have meeting scheduled back to back. A full day will have no fewer than 5 meetings, which is just doable if you don't have more than 30 minutes travel time in between each. My last meeting of the day may include a glass of wine, but otherwise, weirdly, there is no adult refreshment during the course of my day. 50% of the time I have a dinner to go to, and 50% I have a date with room service while I work on all the stuff that didn’t get done while I was flying around like a buzz saw all day.

At some point, either really late at night or super early the next morning, someone calls who has forgotten I’m in another time zone. I tell them it’s fine while wiping sleep out of my eyes and firing up my computer. Hint: I sound unusually perky when you wake me up.

The next day starts with breakfast at 8:00 where one or both people don’t really get to eat because they are trying to do work during the meal. I generally check out of the hotel before this meeting so I’m essentially homeless from now on, and schedule meetings back to back until I get back into a Frito-esque cab to return to the airport.

Flights home seem to have some sort of karma attached that makes them more likely to be delayed. I hang out in the Admiral’s Club doing work that I didn’t get done during the day and listening to other business people talk too loudly into their phones. I eat too many pieces of square cheese and brownie bites.

I finally get home (after dark) and go to bed. The next workday happens 8 hours or less later.

The moral of the story: Business travel? Super sexy. Sorry to spoil your fantasy.

It's kind of weird, you have to admit, that we don't work on a day called Labor Day. But, hey, I'm not one to buck this particular tradition, so there's no blog today.

I'll be back next week with new content, but in the meantime, enjoy the last official day of summer. Have some hot dogs and burgers and raise a glass or keg to one of your favorite alternative investment industry bloggers, even it it's not me. :)

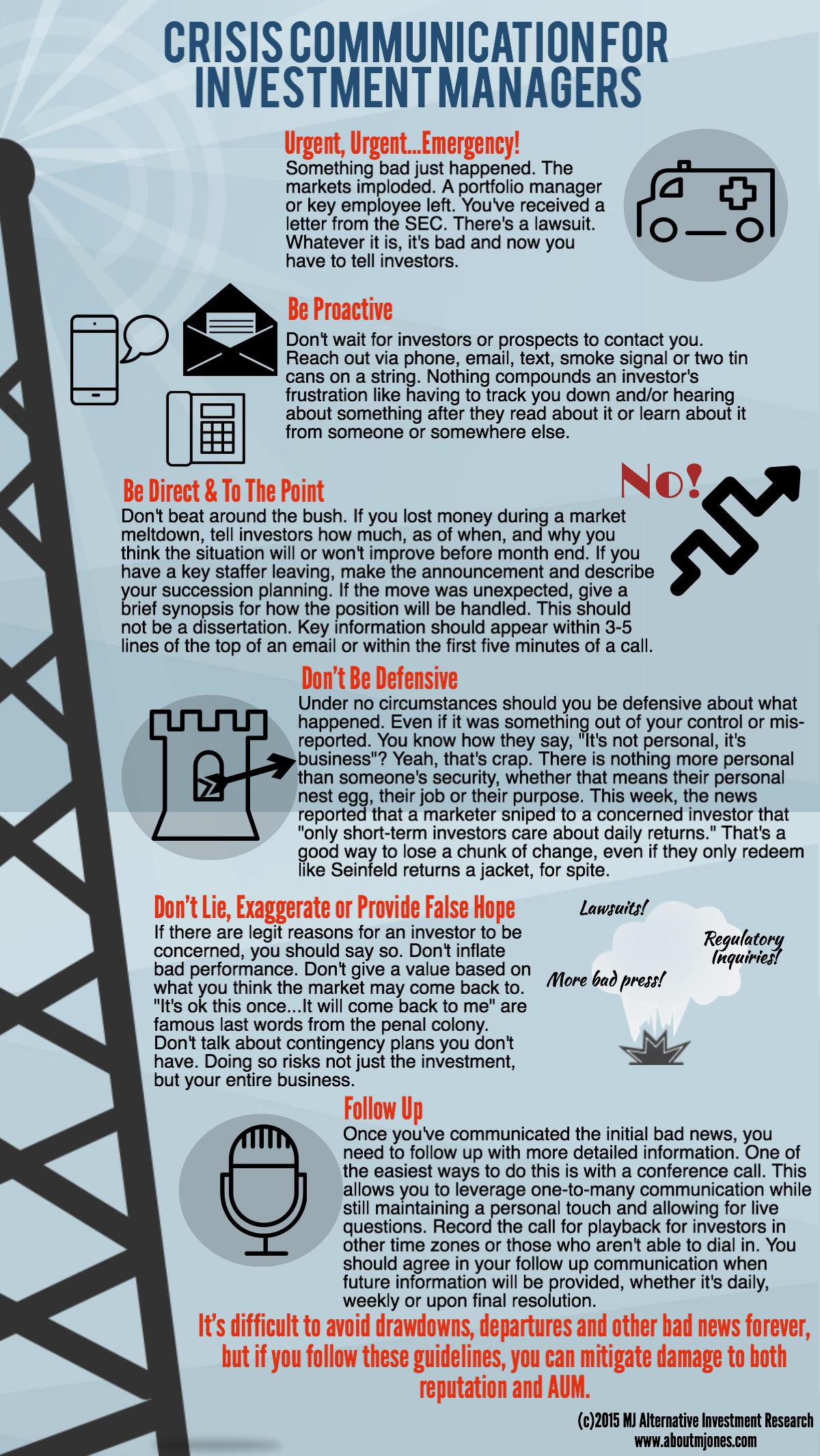

Crisis communications isn't something most money managers practice very often. Well, I guess if they did, they probably wouldn't continue to manage money very long. But last week's market volatility was a great crisis communication "pop quiz" for investment managers. In case you failed the test, or if you just want to boost your score with investors, here are some tips for effectively communicating with investors and prospects during a crisis, whether it's market-driven or created by personnel, regulatory bodies, service providers, or litigation. Communicating effectively during a crisis can make or break a business, so study up and ace the next test.

(C) MJ Alternative Investment Research